One of the most fundamental requirements in managing a qualified retirement plan is counting an employee’s length of service. It is the basis for determining such items as plan eligibility, entitlement to company contributions, vesting and even retirement itself. Although this seems like a straightforward task, the rules are quite complex and create traps for the unwary.

Methods of Counting Service

Before reviewing the reasons for counting service, it is important to understand the methods available for doing so. There are several, and each has certain advantages and disadvantages depending on how a plan sponsor runs its business.

The Elapsed Time Method

The Elapsed Time Method credits an employee for a period of service if s/he is still employed at the end of that period. For example, if Herbert is hired on April 1, 2012, he receives credit for a year of service if still employed on March 31, 2013. Credit is given regardless of the number of hours Herbert works and even if he terminates employment and is rehired prior to March 31, 2013.

One of the advantages of the Elapsed Time Method is that it is not necessary to keep track of actual hours worked. One of the potential disadvantages is that employees who work only limited hours may still be credited with service they would not earn under one of the other methods, entitling them to the same level of benefits as a full-time employee. However, for plan sponsors who seek to benefit all employees equally, this could also be considered an advantage.

The Actual Hours Method

The Actual Hours Method considers the hours that each employee works and/or is entitled to payment, e.g. vacation, sick leave, jury duty, etc. An employee is required to complete a specified number of hours in a period to receive credit for that period. A common example is to require completion of 1,000 hours of service within a 12-month period in order to be credited with one year of service.

Unlike Elapsed Time, this method requires employers to keep and review records of the actual time each employee works. For hourly-paid employees, records are already available, so there would be minimal additional recordkeeping. For salaried employees, the Actual Hours Method will likely impose added recordkeeping. One of the advantages of this method is that it requires all employees to work the same minimum hours of service to be entitled to the same level of benefit under the plan.

The Equivalency Method

This method is a hybrid of the first two. It credits employees with a certain number of hours for each period they work as follows:

- 10 hours per day

- 45 hours per week

- 95 hours per semi-monthly pay period

- 190 hours per month

For a plan that uses the monthly equivalency, an employee who performs any service in a month is treated as working 190 hours during that month. If the plan credits a year of service as described above, i.e. 1,000 hours in a 12-month period, an employee would need to perform at least one hour of service in at least six out of the 12 months (six months x 190 hours per month = 1,140 hours) to earn a year of service. The Equivalency Method has the advantage of requiring continuous service while minimizing additional recordkeeping requirements; however, similar to the Elapsed Time Method, it can still have the effect of crediting very limited time employees with the same benefits as full-time workers.

Reasons for Counting Service

Now that we have reviewed the methods, it is time to cover some of the reasons why properly counting service matters.

Initial Plan Eligibility

Many plans require employees to satisfy certain age and/or service requirements to become eligible. If there is a service requirement, the plan must specify how to determine when an employee has satisfied it. In plans that use the Elapsed Time Method for eligibility, measuring the service requirement can be straightforward. For example, if a plan requires employees to complete six months of service to be eligible, any employee who remains employed six months after his/her hire date has satisfied the service requirement as of that date. Similarly, if the plan requires completion of one year of service, employees satisfy the requirement if they are still employed a year after they are hired.

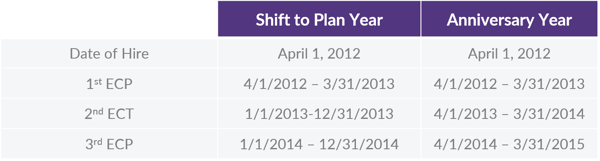

There are some additional complexities for plans that require completion of a minimum number of hours as part of the service requirement. Keep in mind that the hours component may be reviewed based on either actual hours worked or an equivalency. Consider a plan with a requirement of one year of service, defined as completion of 1,000 hours in a 12-month period. With a few very limited exceptions, this is the maximum service requirement a plan can impose. One of the first items to identify is the 12-month period used to measure the hours worked. This is called the Eligibility Computation Period (ECP). In this scenario, an employee’s first ECP always runs from initial date of hire to the first anniversary date; however, the plan must specify whether the second and all subsequent ECPs shift to the plan year or continue to follow employment anniversary dates.

Let us return to our friend Herbert.

If Herbert does not complete at least 1,000 hours of service by March 31, 2013, his eligibility service will be measured either during the 2013 calendar year or his second employment anniversary year, depending on the ECP specified in the plan document, to determine if he meets the service requirement. Note that when the ECP shifts to the plan year, the period from January 1, 2013 through March 31, 2013 is counted in both the first and second ECPs; therefore, any hours Herbert works during that timeframe must be included in both ECPs when assessing whether he completed the requisite 1,000 hours.

Many employers find the plan-year-shift method to be much easier to manage since all employees will be tracked during the same 12-month period (the plan year) after their initial year of employment. For plans that continue to use anniversary year, each employees’ hours must be tracked over a different 12-month period, depending on their dates of hire — a requirement that can be quite burdensome and time-consuming.

Plans with shorter service requirements can also face challenges when incorporating an hours-worked component. Recall that the maximum service requirement allowed by law is 12 months with 1,000 hours. That means a plan with a service requirement of completion of three months with at least 300 hours would be in violation since an employee could complete 1,000 hours in a year without ever working 300 hours in three months. Therefore, extreme caution should be exercised when establishing service requirements of less than one year that also incorporate hours.

Also, consider a plan that requires completion of six months of service with at least 500 hours of service. Depending on how the plan document is written, this provision could impose burdensome recordkeeping requirements. For example, it may refer to contiguous 6-month periods, e.g. January 1 to June 30 followed by July 1 to December 31, or it may create rolling six-month periods, e.g. January 1 to June 30 and February 1 to July 31, etc.

Regardless of how a plan counts service for eligibility, it is important to remember that all service dating back to an employee’s original hire date must be considered.

Vesting

While not quite as complex as eligibility, counting service for vesting has a few noteworthy nuances. Similar to eligibility, the plan must specify which counting method (Elapsed Time, Actual or Equivalency) is to be used and define the measurement period (Vesting Computation Period or “VCP”) as either the plan year or anniversary year. Unlike eligibility, however, the VCP does not shift after the initial year. It is either always the plan year or always the anniversary year. For plans defining the VCP as the plan year and using the Actual Hours or Equivalency Methods, new employees effectively have fewer than 12 months to complete the required hours to earn a year of vesting service during the initial VCP. When the VCP is the anniversary year, plan sponsors should be aware of the same recordkeeping burden as described for eligibility. Namely, when using Actual Hours or Equivalency, each employee will have a different tracking period based on his or her hire date.

There is another very key area in which eligibility and vesting are different when there is an hours-worked component involved. Let us again consider a plan that requires completion of 1,000 hours in a 12-month period to be credited with a year of service. For eligibility, both of these requirements must be met; an employee must complete both 1,000 hours of service and 12 months of employment before being credited with a year of service. An employee who works well over 1,000 hours but terminates employment after only 11 months does not receive credit.

For vesting, on the other hand, an employee is credited with a year of service as soon as he or she completes 1,000 hours of service during a VCP regardless of the number of months worked. Therefore, it is not at all uncommon for an employee to have received credit for more years of service for vesting that for eligibility/participation. This is especially important to remember when determining vesting credit for an employee who terminates but may have already completed 1,000 hours prior to termination.

One other important difference is the years that must be counted for vesting. Although all service from date of hire must be recognized for eligibility, a plan can be written to ignore years prior to its effective date (or the effective date of any previous plans) and/or years prior to attainment of age 18 for vesting purposes.

In addition to eligibility and vesting, there are several other provisions that may require counting service. Examples include

- Allocation requirements, such as completion of a year of service, to share in allocations of matching or profit sharing contributions for a year, and

- Definitions of normal retirement using both age and service such as later of attainment of age 65 or completion of five years of service.

Conclusion

While there is flexibility to count service using any of the methods described above, plan documents must specify the methods a plan elects to use; therefore, it is advisable to review plan documents regularly to ensure proper understanding and to seek assistance from service-providers to clarify any points of confusion. For more information on retirement plan design, visit our Knowledge Center here.