Plan Loan Guide")

So, your plan allows loans. Simple enough, right? Participants borrow money from their accounts and pay it back. Why does that have to be complicated?

The reason is that a participant loan, at its core, is an exception to a rule. One of the main federal laws that govern retirement plans was put in place to protect the assets in those plans and prevent plan officials from using plan assets for less than honorable purposes. One way of doing that was to impose a prohibition on loaning any plan money to interested parties.

Participant loans are an exception to that broad prohibition. As long as certain limitations and parameters are satisfied—amount, duration, interest rate, etc.—an otherwise impermissible loan becomes OK. But, because of the way the rules are written, there is no such thing as “close enough.” In order to make a prohibited loan acceptable, every single requirement must be satisfied, and that is where things can get complicated.

Don’t believe us? Let’s play a game of twenty questions!

Do all plans have to permit participant loans?

Not at all. This is a completely optional provision, and each plan sponsor can decide for itself whether offering a loan provisions makes sense. That decision is reflected in the plan document.

Are there any parameters that apply to participant loans?

There are some outside parameters, but each plan sponsor can customize its loan offering within those bookends. Once customized, the specifics must be documented in a formal, written loan policy and disclosed to plan participants.

We will review some of the parameters in more detail throughout this FAQ, but they focus on the interest rate, payment frequency, amount, and duration.

Can a plan set a minimum loan amount?

The rules do not require a minimum loan amount, but plans are able to set one so that participants are not continually asking for loans for small amounts. As a general rule, a minimum of $1,000 or less is considered acceptable. Anything above that is generally considered discriminatory because it could disproportionately limit loan availability to lower-paid participants who are likely to have smaller account balances.

Is there a cap on how much a participant can take as a loan?

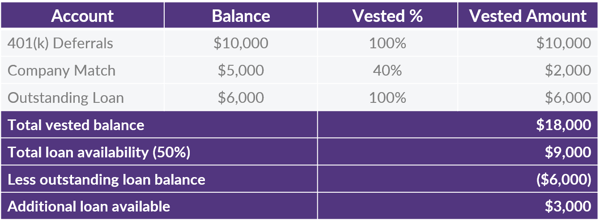

The maximum is a little more involved. The rules indicate that a participant can take out up to 50% of his or her vested account balance, subject to an overall cap of $50,000. This is a straightforward calculation for someone who has not taken out any previous loans, but it can get tricky when prior loans must be considered.

For starters, a loan is still considered part of a participant’s balance and must, therefore, be considered if someone with a loan requests a second loan. Here is an example. Norma is a plan participant with the following account:

The other tricky part of the calculation is that the $50,000 overall cap is reduced by the highest outstanding loan balance a participant had during the 12 months just before requesting the loan.

Let’s look at another quick example. Cooper has a large enough vested account balance that his maximum loan amount is based on the $50,000 cap and not the 50% limit. He takes out a plan loan for $40,000 on January 31, 2018. It is only a short-term need, and Cooper completely repays the loan on September 1st of that same year. Fast forward to December 1st, and Cooper realizes he needs some additional cash and probably shouldn’t have been so quick to repay his plan loan. The maximum he is able to take out is now reduced to only $10,000, as follows:

Maximum loan amount: $50,000

Highest outstanding balance during previous 12 months: $40,000

Amount available for a new loan: $10,000

Cooper will continue to be limited on how much he can take as a new loan until September 1, 2019 (12 months after the date the prior loan was fully repaid).

That sounds complicated. Can a plan limit how many or how often loans can be taken?

Most definitely. There is no regulatory limit on the number of loans – only the maximum dollar amount – but plans are free to impose such a limit. It may be a limit on the number of outstanding loans at any one time or a wait from the time one loan is repaid until a new loan can be taken or just about anything in between.

Keep in mind, however, that the more limitations that are imposed, the more diligent everyone must be to ensure those limits are consistently applied.

The most common provision we see is to limit participants to one loan at a time.

Is it possible for a participant to refinance an existing loan?

Yes, as long as the plan allows for it. But there are some important caveats here. First is that many loan policies do not overtly say whether or not loan refinancing is permitted. In those cases, we have to get into the regulatory weeds. The rules indicate that when a participant refinances a loan, two loans actually exist for a moment in time. There is the loan being replaced and there is the loan doing the replacing. So, if a plan limits a participant to only one loan at a time but does not make a specific exception for refinancing, then it would be a violation of the “one at a time” restriction to allow a participant to refinance a loan.

The second item is that there are some convoluted calculations that can further limit whether a participant can refinance an existing loan. Because those calculations make the Norma and Cooper examples look like a walk in the park, we won’t go into the details here, but suffice it to say that it can get quite complex and confusing.

The third caveat, and one we see overlooked fairly often, is that any change to a material loan term is technically a refinancing even if a participant does not take out any more money. Think of it in terms of a home mortgage. If the homeowner wants to take advantage of a lower interest rate, he or she can’t just call the bank and ask for a new amortization schedule. It requires the loan to be completely refinanced. Plan loans are the same in that respect. So, any request to change an existing loan must be reviewed against the refinancing rules rather than simply preparing a new amortization schedule.

You mentioned interest rates. How does a plan determine which rate to use for a participant loan?

The Department of Labor defines reasonable rate of interest as a rate that “provides the plan with a return commensurate with the interest rates charged by persons in the business of lending money for loans which would be made under similar circumstances.”

Rather than calling several local banks to inquire about current rates every time a participant asks for a loan, many plan sponsors write into their loan policy that will use a factor of the current Prime rate – usually Prime plus one or two percent. The Prime rate is the interest rate banks charge their most creditworthy customers. Adding one or two percent makes the interest rate charged to the participant more consistent with general consumer rates, as individuals can rarely get a loan at the going prime rate.

What is the longest period of time a loan can be outstanding?

The rules limit general purpose loans to a maximum of five years; however, if the participant is using the loan proceeds to purchase his or her primary residence, the loan can be extended to the length of the first mortgage. It is common for plans to limit residential loans to no more than 10 years.

As with all of these parameters we are discussing here, the loan policy should spell out these details.

How and when are loans repaid?

The rules provide that level payments must be made at least quarterly. It is common practice, however, for plans to require participants to repay their loans through payroll deduction. That means when a participant takes a loan, it is amortized assuming a payment will be automatically withheld from each paycheck. If actual payments do not follow that schedule every step of the way, it can create compliance headaches for the plan and trigger tax liabilities for the participant.

What happens when an employee wants to pay off their loan early? Can they?

That is up to the plan’s loan policy. Most of them allow a participant to repay a loan in full at any time. Since it would be a bit unusual for someone’s paycheck to be large enough to do this via payroll deduction, it is one of the few times a plan might accept separate payment. Many plans choose to require some sort of certified funds to avoid the risk of dealing with potential insufficient funds issues if the participant pays via personal check.

Making extra periodic payments is a completely different discussion. Each time additional payments are made, the “extra” should be applied directly to the outstanding principal balance of the loan. That means the breakdown of principal and interest changes for each subsequent payment. Since many recordkeepers do not have the ability to make these sorts of adjustments “on the fly,” we generally suggest that these sorts of extra payments not be permitted.

How do we handle a missed payment?

A payment could be missed for any number of reasons – anything from an hourly employee not having a paycheck from which to withhold a scheduled payment to simple administrative oversight. Regardless of the reason, a missed payment means the loan is in default, and steps must be taken to get it back on track as quickly as possible. Options vary but could include doubling up on withholding (plus accrued interest) on the next paycheck to potentially refinancing the loan if the plan allows it. If missed payments are not caught up by the end of the following quarter, the outstanding balance must be treated as a distribution to the participant, resulting in taxes and penalties.

If an active employee wants to discontinue their payments, can I say yes?

The short answer is “No.” The longer answer is that one of the underlying requirements for a loan to be permitted is that it must be an enforceable agreement, and plan fiduciaries have a legal obligation to enforce a plan’s agreements and collect amounts that are owed to the plan. That means once a participant has agreed to repay the entire loan, it becomes a plan fiduciary’s duty to make sure that happens. To voluntarily discontinue payments on a participant’s request would be a violation of that duty. However, if a participant will be out of work on an approved formal leave of absence, payments can be temporarily suspended. There are a lot of details on how that works, so give us a call if you are facing that situation, and we can help you understand the options.

What happens when a participant with an outstanding loan terminates employment?

Most plans include a provision that makes outstanding loans due immediately on termination of employment. Since the participant in question no longer has a paycheck from which to withhold payments, the pay-off is made via personal check or money order. If it is not repaid, it is treated as a taxable distribution to the participant. Early withdrawal penalties may also apply.

A participant has informed the company that they have filed for bankruptcy. Does that impact participant loan payments?

The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 provides that the obligation to repay a participant loan from an employer-sponsored retirement plan is not affected by a bankruptcy filing. Not only must a participant continue to make regularly scheduled payments pursuant to the original loan agreement, but the amount of the regular payment is deducted from that individual’s income in establishing whether or not the needs-based test is satisfied for discharge of other debts.

You’ve made a couple of comments about loans being treated as distributions. How does that work?

The so-called “deemed distributions” rules are kind of like falling out of a window. No one has to take any action to make gravity work…it just does. Same with a loan that is behind and not caught up by the end of the next quarter…it is automatically deemed to be a taxable distribution whether anyone reports it as one or not. Obviously, the plan has a duty to document it, but failure to do so doesn’t mean the tax liability isn’t there.

The participant must be issued a Form 1099-R, reporting the outstanding balance as a taxable distribution. The deadline for the 1099 is the January 31st immediately following the year of the deemed distribution. Although plan recordkeepers can usually provide this service quite easily, they typically require a plan sponsor to request it for each applicable loan. In other words, recordkeepers often do not issue 1099s for deemed distributed loans automatically.

Although this should primarily involve terminated employees, it is possible that an active employee could end up with a deemed distributed loan as well. However, since payments should not be voluntarily discontinued for an active employee, please call us if this situation arises so we can make sure there are not any other compliance issues that need to be addressed.

Can I deny a loan request?

It depends. We know, that’s a cop-out answer, but it’s true. Certainly, if the request is outside the plan’s loan rules, it should be denied. Also, if you have knowledge that a participant is using the loan option as a way to access his or her account and has no intention of repaying the loan, that could be grounds for a denial. Beyond that, it is difficult to think of a circumstance when it would be appropriate to deny a legitimate request.

It is important to note that loans must be offered on a nondiscriminatory basis. In other words, it would be a violation to deny a loan to a non-highly compensated employee but approve a request by an HCE under similar circumstances. As with pretty much all plan-related decisions, keeping documentation as to why a loan is denied is a must.

This is way more involved than I realized. Should I even allow loans in the plan?

While loans may seem like they are more trouble than they’re worth, think about the alternative. An employee may instead take a distribution, which will never be repaid. The money is gone and will not be available when the participant retires. With a loan, the funds are eventually returned to the plan.

What do I do if I have more questions about loans?

OK, that only makes 17 questions, but this is the easiest one to answer. Contact DWC!