Plan Sponsor Requirements

With all the different deadlines (depending on the reason and type of contribution), it is no wonder this topic can be cause for confusion.

Employee Deferrals The deadline to deposit an employee deferral and/or participant loan payment is generally two to seven business days following each pay date. There are certain very rare instances that allow more time (subject to an outside limit), but they are few and far between. If someone tells you that you have until the middle of the following month, get a second opinion.- Company Contributions For tax-deductibility, companies must deposit matching and profit-sharing contributions no later than the due date (including extensions) of the company tax return. However, there are some other deadlines that might apply. For example, certain safe harbor matching contributions are subject to a quarterly deposit deadline.

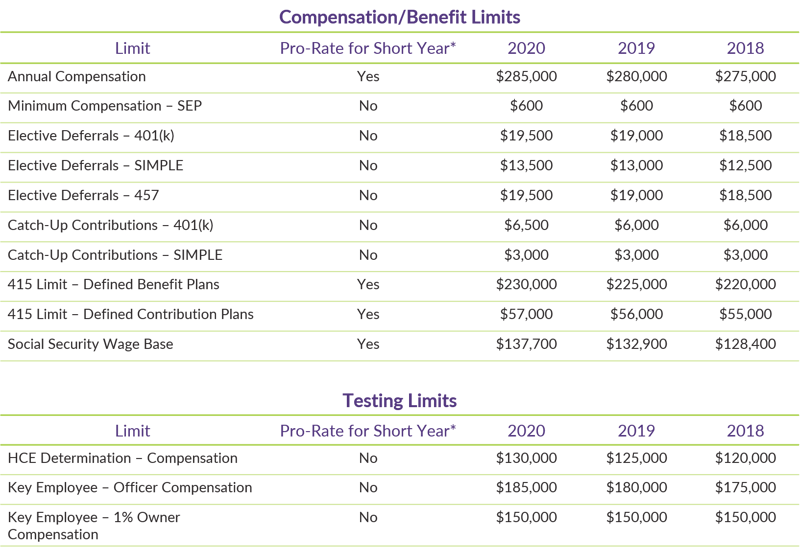

There are also specific retirement plan contribution limits that must be adhered to:

*For a plan year that is less than 12 months (either due to initially establishing the plan after the first of the year or terminating a plan before the end of the year), these limits must be pro-rated based on the number of months in the short plan year. For example, a plan year that runs from January 1st through September 30th would multiply the applicable limit by 9/12.

To see a chart of historical contribution and testing limits data, click here.